Car Lease Buyout in 2026: When It’s a Smart Win Vs a Money Trap

Try standing at the crossroads. On one side, your leased car—a familiar ride that's survived pandemic chaos, inflation, and a market gone berserk. On the other, a world of sticker shock: new vehicles priced like condos, used car lots stripped bare, and dealers who seem to change the rules mid-game. Welcome to the car lease buyout decision in 2025, where every move matters, and even the sharpest drivers can get blindsided. In this no-fluff guide, we dive into the real risks, the overlooked rewards, and the expert strategies that could save (or lose) you thousands. If you're teetering on the edge of a lease, or just want to outsmart a system that's always shifting, buckle up. This is the brutal, data-driven, and slightly provocative truth about car lease buyouts right now.

Welcome to the edge: why car lease buyouts matter now

The post-pandemic market: why everything changed

A few years ago, car leases were predictable: drive, return, repeat. COVID-19 changed all that—supply chain chaos, chip shortages, and rolling factory shutdowns torched the old rules. Dealerships emptied out almost overnight, and used cars suddenly became gold. Lessees found themselves sitting on hidden equity, often without realizing it—sometimes the buyout price written into a contract years before was suddenly a bargain compared to a red-hot market.

By 2024 and 2025, this volatility had turned lease buyouts from a niche move into a mainstream power play. According to Lease End’s 2025 report, consumer savings from buyouts reached $75.7 million in 2024 alone, and the trend shows no sign of cooling off. New car prices hit an average of $48,641 in March 2025, while monthly lease payments ballooned past $700. The result? A massive uptick in lease buyouts, especially as new vehicle supply lags and automakers like Tesla reinstate buyout options after prior restrictions.

| Year | Used Car Value Spike | Lease Buyout Trend | Notes |

|---|---|---|---|

| 2020 | +18% | Low | Pre-pandemic market |

| 2021 | +36% | Moderate | Chip shortage begins |

| 2022 | +22% | High | Severe supply crunch |

| 2023 | +9% | Very High | Buyouts surge |

| 2024 | +6% | Peak | Record consumer equity |

| 2025 | +2% | Still strong | Supply slowly recovers |

Table 1: Timeline of used car value spikes and lease buyout trends, 2020-2025. Source: Lease End 2025 Report

Who’s searching for a car lease buyout—and why

Lease buyouts attract a very particular crowd: drivers who want to keep what works, escape dealership games, or spot an arbitrage opportunity. Pain points? Plenty. Fear of overpaying, confusion about hidden fees, anxiety over vehicle condition, and the emotional weight of making a mistake on a five-figure decision. It’s no surprise that Millennials and Gen Z are leading the charge, with buyout activity jumping from 35% to 47% among these groups between 2022 and 2024.

Here’s what the “experts” rarely mention about car lease buyouts:

- You can sometimes buy at below-market value: If your contract’s buyout price was set years ago, it may be a bargain now—provided the market hasn’t cooled dramatically.

- Positive equity is real: With tight used car inventory, many drivers discover they can buy out and sell for a profit, pocketing the difference after taxes and fees.

- No more surprise wear-and-tear charges: Buying out your lease means you skip dealer inspections and penalty fees for minor dings or over-mileage.

- Zero sales pressure: No awkward negotiations about your next car, no upselling—you control the process.

- Direct financing is available and competitive: Lease buyout loans often start at just 5% APR, with minimums as low as $2,500.

- You keep the car you know: No surprises about reliability, service history, or hidden damage.

- You avoid the new car lottery: In a market where new models can be delayed for months, keeping your current ride can be the logical—and stress-free—answer.

But there’s a catch. For every driver at this crossroads, there’s a knot in the stomach: “What if I’m missing something?” That uncertainty—the fear of hidden traps or leaving money on the table—is what makes the car lease buyout decision both an emotional and financial minefield.

How the car lease buyout process really works (no B.S.)

Decoding your lease contract: what to read between the lines

Most drivers sign their lease contract and promptly forget it. That’s a mistake—every critical buyout variable is buried in that dense paperwork. The fine print determines your destiny, not the dealer’s handshake.

Key contract sections to scrutinize:

- Residual value: This is the predetermined value of your car at lease end. It’s the backbone of your buyout price—if it’s lower than current market value, you’re already winning.

- Purchase option price: This is the price you’ll pay to keep the car. Sometimes it’s residual plus a small fee, sometimes it sneaks in hidden add-ons.

- Disposition fee: The dealer’s “thanks for playing” charge if you return the car instead of buying it. Watch out—this fee disappears if you buy, boosting your math.

- Mileage and wear-and-tear stipulations: Overages can cost you if you return the vehicle, but buying it out lets you sidestep those penalties.

Definition list:

The estimated wholesale value of the car at lease end. Set by the leasing company at contract signing, it can be your ticket to equity or a reason to walk away if set too high.

A charge (often $350-$500) assessed if you return the car at lease end. Avoidable if you buy the vehicle, but always read the fine print—some contracts sneak in an “early buyout” fee.

The sum you pay to buy the car. Typically residual value plus any purchase option or administrative fees. This figure is crucial; compare it against live market valuations (Kelley Blue Book, Edmunds, futurecar.ai) before making a move.

Step-by-step: how to execute a car lease buyout in 2025

If you’re serious about a car lease buyout, here’s how to master the process—no corporate fluff, just actionable steps:

- Pull your lease contract and find the purchase option price.

- Check your car’s current market value on multiple platforms (KBB, Edmunds, futurecar.ai).

- Factor in fees: Add any purchase option, administrative, or state-mandated costs.

- Assess vehicle condition: Honest self-inspection is a must—document everything.

- Calculate equity: If market value > buyout price + fees, you’ve got positive equity.

- Shop for buyout financing: Compare credit unions, major banks, and online lenders—rates start near 5%.

- Contact your leasing company: Request a formal payoff quote and clarify payment logistics.

- Negotiate any dealer buyout fees: Dealers hungry for business may waive or reduce these costs.

- Finalize your financing and arrange payment: Follow lender and lessor instructions to the letter.

- Transfer title and register: Complete all required paperwork to make the car officially yours.

Alternatives to this direct approach include having a dealer facilitate the buyout (sometimes easier but can cost more) or working through a third-party like Lease End or dedicated buyout services for added transparency.

| Buyout Method | Pros | Cons | Typical Extra Costs |

|---|---|---|---|

| Dealer buyout | Simplifies paperwork; dealer handles DMV | Higher fees; potential markups | $300–$900 |

| Direct lender | Lowest cost; most control | You do legwork; longer wait times | $150–$400 |

| Third-party facilitation | Easiest for busy drivers; transparency | Service fees; limited flexibility | $250–$700 |

Table 2: Comparison of dealer buyout vs. direct lender vs. third-party buyout. Source: Original analysis based on LendingTree, Car and Driver.

What you need before starting (and what to avoid)

Preparation makes all the difference. Here’s what you need—plus the traps to sidestep:

- Your original lease contract (physical or digital copy)

- Current vehicle registration and proof of insurance

- Payoff statement or formal buyout quote from the lessor

- A confirmed financing offer (unless paying cash)

- State-specific forms for title transfer and tax calculation

- Identification and all keys/fobs

Red flags to watch out for when buying out your lease:

- Unexpected administrative fees: Sometimes slipped into buyout paperwork—always ask for an itemized breakdown.

- High dealer facilitation charges: Dealers may double-dip on fees, especially if you’re not buying another car from them.

- Ballooning interest rates: Some lenders mark up APRs on lease buyout loans—compare at least three offers.

- Missing paperwork: Incomplete forms delay title transfer, risking extra fees or penalties.

- Title transfer delays: Some states are notoriously slow—build in extra time.

- Early buyout penalties: If you’re pre-maturity, verify whether your contract allows this (and at what cost).

The most common mistakes? Failing to read the contract, overestimating the car’s resale value, underestimating taxes and fees, and accepting the first financing offer. Knowledge and skepticism are your best defense.

The myth-busting zone: common misconceptions debunked

Top 5 myths about car lease buyouts

The internet is a breeding ground for bad advice. Here are the five most persistent myths, with a reality check attached:

- Myth: The buyout price is always a rip-off.

Reality: In 2025’s market, many contracts are netting buyers thousands in positive equity. - Myth: You can’t negotiate fees or terms.

Reality: Dealers and lessors often bend on fees—especially if you threaten to walk. - Myth: Early buyouts are never allowed.

Reality: Most leases allow early buyouts, but expect penalties or adjustments; read the fine print. - Myth: Only cash buyers can do a buyout.

Reality: Specialized lease buyout loans are widely available, sometimes with better rates than standard auto loans. - Myth: Buyouts kill your credit.

Reality: Lease buyouts can impact your credit, but typically less than missing payments or rolling negative equity into a new lease.

"People think the buyout price is set in stone. It rarely is." — Alex, Automotive Analyst, 2025

What the fine print really means (and what they hope you miss)

Don’t let legalese lull you into submission. Buried in leases are clauses about excess mileage, early termination, and mandatory inspection fees. Some dealers bank on you missing these—others quietly add “reconditioning” or “processing” charges at buyout.

If you spot a questionable fee, challenge it. Bring your research (use resources like futurecar.ai and government consumer protections), call out discrepancies, and don’t be afraid to escalate. Negotiating these fees upfront—before paperwork is signed—often yields the best results.

Money on the line: hidden costs, surprise fees, and how to outsmart them

The real cost breakdown: what you’ll actually pay

The sticker buyout price is just the start. Add in purchase option fees, state sales tax, administrative costs, and the possibility of unexpected charges. According to LendingTree, average total buyout fees in 2025 range from $350 to $1,200, with taxes adding another 6–10% depending on your state.

| Cost Component | Typical 2025 Amount | How to Avoid or Reduce |

|---|---|---|

| Purchase option fee | $200–$600 | Negotiate or seek lender waivers |

| Administrative fee | $50–$250 | Request itemized breakdown |

| Dealer facilitation | $300–$900 | Self-handle paperwork, compare |

| State taxes | 6–10% of buyout | Check for credits on trade-ins |

| Title/registration | $100–$350 | Verify with local DMV |

| Disposition fee | $350–$500 | Waived if you buy |

Table 3: Hidden fee matrix and tips for lease buyout cost avoidance. Source: LendingTree, 2025.

Time your buyout strategically—some states pro-rate taxes based on registration period, while others credit you for trade-ins. Always verify with your local DMV and lessor.

Negotiation dark arts: insider tactics and traps

Dealers know most buyers are anxious to wrap up their lease and move on. They’ll use this urgency against you, introducing last-minute “mandatory” services, unnecessary inspections, and “expedited processing” fees.

"If you don’t ask, you’re paying their vacation fund." — Pat, Consumer Advocate, 2025

Common dealer tactics in buyout negotiations:

- Bundled fees: Dealers combine legitimate and questionable charges—demand an itemized list and challenge anything suspicious.

- “Mandatory” inspections: Some insist on extra inspections for a buyout—rarely required if you’re not returning the car.

- Financing markups: Dealers offer in-house financing at inflated rates; always bring your own pre-approval.

- Scarcity messaging: “We’re seeing a lot of demand for this car”—classic pressure tactic, often exaggerated.

- Delayed paperwork: Dragging out the process to induce urgency—stay calm and document all communications.

When a lease buyout is a terrible idea (and what to do instead)

Car lease buyouts don’t always make sense. It’s usually a bad move if:

- Your buyout price is thousands above current market value—even with fees, selling privately would net you less.

- The car has major mechanical issues or a questionable maintenance history.

- You’re rolling negative equity into new debt, risking an “underwater” loan.

Alternatives? Walking away and absorbing the disposition fee (sometimes cheaper), swapping the lease with an interested party, or refinancing through a lower-rate lender. Each option has trade-offs—compare all costs before pulling the trigger.

And if you’re still undecided, ask yourself: “Am I buying certainty, or just avoiding a tough decision?”

Case studies from the front lines: real people, real results

The jackpot: how one buyer made $4,000 on her lease buyout

Meet Jordan. In early 2025, she faced a $19,500 buyout on a leased Honda CR-V. Market value? $23,500. After closing costs and taxes, she sold the car privately for $23,000 and pocketed a cool $4,000. Her edge? Diligent research, fast action before market shifts, and negotiating dealer fees down to zero.

Jordan’s step-by-step:

- Checked contract to confirm a low residual value

- Compared prices on futurecar.ai/compare-vehicles and Edmunds

- Arranged buyout financing at 5.1% APR

- Insisted on a fee breakdown and challenged unnecessary charges

- Sold the car within a week—maximizing her equity

Lesson: The window for positive equity is narrow. Act fast, verify every fee, and don’t assume the dealer’s first answer is their best.

The nightmare: when a buyout backfired (and how to recover)

Then there’s Sam. He rushed into a buyout, ignoring a nagging check engine light and neglecting to check the car’s declining market value. After fees and a costly repair, he realized he’d paid nearly double the car’s worth.

What went wrong? Ignoring independent inspections, skipping market value checks, and failing to negotiate. Sam’s path to recovery involved refinancing the remaining loan at a lower rate, cutting his losses by selling to a private party, and sharing his hard-won lessons online.

"I thought I was saving money—turns out, I paid double." — Sam, Private Seller, 2025

The middle ground: playing the long game

Finally, Morgan’s story: Her buyout netted no windfall, but she avoided ballooning lease payments and kept a car she trusted. By timing the buyout during a lull in market prices and leveraging a pre-approved loan, she minimized costs and headaches.

The differentiator? Timing, diligence, and a willingness to walk away if the math didn’t add up. The majority of buyers land here—no big win, no disaster, just a smart, measured move that fits their needs.

Advanced strategies: maximizing value and minimizing regret

Timing is everything: when to pull the trigger

In a volatile market, timing your buyout is as critical as the decision itself. Used car prices in 2025 remain high due to supply shortages, but regional dips can occur. According to MSN, holding out for a market lull or acting before another price spike can shift the equity equation by thousands.

| Buyout Timing | Avg. Market Value Retention | Equity Outcome |

|---|---|---|

| 90 days pre-maturity | 98% | Moderate |

| At maturity | 100% | Highest |

| 90 days post-maturity | 95% | Lower |

Table 4: Statistical summary of buyout timing versus market value retention. Source: Original analysis based on MSN Auto, 2025.

Tactical tip: Monitor market prices weekly, and don’t hesitate to move quickly if your contract and local laws allow. Use futurecar.ai and other real-time tools to track trends and spot your moment.

Financing your buyout: what the banks won’t tell you

Lease buyout loans are their own beast. Rates start around 5%, but some lenders quietly tack on extra requirements—think higher minimums, mandatory inspections, or origination fees. Read every disclosure, and always compare at least three lenders.

Avoid “underwater” loans by borrowing only what the car is truly worth—don’t roll in negative equity from another vehicle unless you want a debt spiral.

Definition list:

Annual Percentage Rate—the true cost of borrowing, including fees. A low APR can save thousands, but hidden charges add up fast.

Owing more than your car is worth—a dangerous position if market values drop or you need to sell suddenly.

A large final payment at the end of the loan term. Sometimes used to lower monthly payments, but can create a nasty surprise if you’re not prepared.

Lease buyout and your credit: the untold impacts

Lease buyouts can ding your credit score—especially if you miss a payment or take on too much debt. But managed wisely, they can actually help by adding a new installment account and building payment history.

To minimize negatives: Pay off other debts first, avoid maxing out your credit, and don’t open multiple loan accounts at once. Check your credit report for errors before applying and shop for buyout loans within a short window (14-30 days) to minimize scoring impact.

Beyond buyout: what’s next in car ownership and mobility?

Alternatives to traditional buyout: subscription, swap, or walk away?

The world doesn’t end at buyout. Subscription services, lease swaps, and simply walking away are all on the table in 2025. Here’s how to decide:

- Evaluate your buyout price versus market value.

- Estimate total fees and taxes.

- Compare flexible subscription or swap programs for monthly cost and convenience.

- Assess your future driving needs—do you need the same car, or are your habits changing?

- Calculate the true cost of walking away—including disposition fees and lost equity.

- Consult expert resources (like futurecar.ai) for up-to-date market trends and side-by-side analysis.

A systematic approach ensures you’re not leaving money—or opportunity—on the table.

The cultural shift: why ownership isn’t what it used to be

Car ownership in 2025 is as much about identity as transportation. Urbanization, hybrid work, and a growing appetite for sustainability are all pushing drivers to rethink old assumptions. Shared vehicles, subscription models, and on-demand access are chipping away at the “I must own my ride” mindset.

For many, a lease buyout is less about the car itself and more about control, autonomy, and flexibility in a turbulent world.

Where experts see the future of car leases

Insiders agree: The golden age of lease buyout arbitrage won’t last forever. As supply chains recover and residual value models get smarter, the easy wins may dry up. But for drivers who stay informed and act decisively, opportunities will always exist.

"Buyouts won’t always be a goldmine. The game is changing fast." — Alex, Automotive Analyst, 2025

To stay ahead: Regularly monitor market trends, leverage AI-powered research tools, and never stop questioning dealer narratives.

Power tools: checklists, guides, and resources

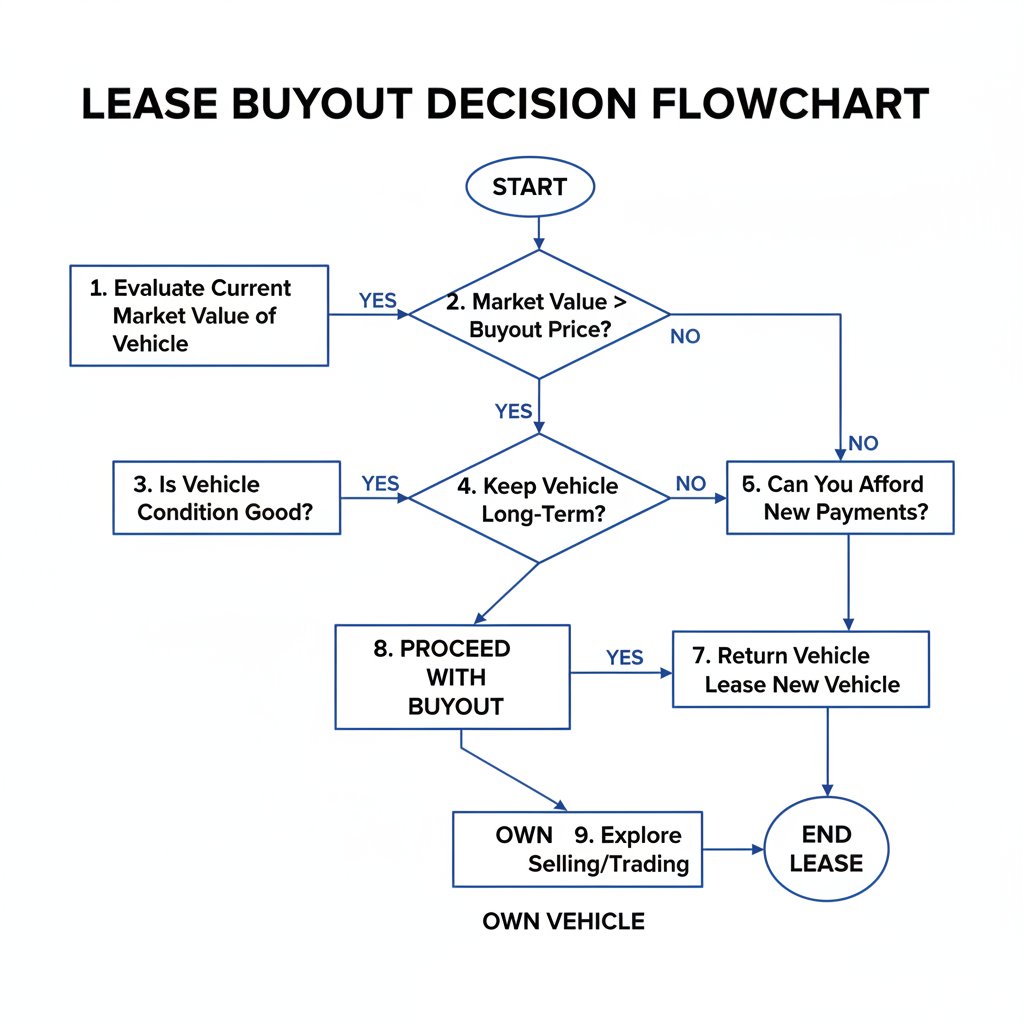

Quick reference: your lease buyout decision flowchart

Use this flowchart as your sanity check: Are you buying for value, convenience, or emotion? Does the math work at every step? Cross off each box before signing anything.

Must-ask questions before you sign

- What is my exact buyout price, including all fees and taxes?

Knowing the full number stops nasty surprises later. - How does this price compare to my car’s current market value?

Equity only matters if you verify the data. - Are there any early buyout penalties or restrictions?

Hidden clauses can wreck even the best deals. - Does my state charge sales tax on the lease buyout?

Tax rules can swing the math by thousands. - Am I eligible for buyout financing, and what’s the true APR?

Shop around—don’t get locked into dealer rates. - Will any fees be waived if I buy directly from the lender?

Sometimes skipping the dealer saves big bucks. - What paperwork and timelines are required for title transfer?

Delays here can cause cascading headaches.

Asking these questions upfront can save you money, stress, and a mountain of regret.

Expert resources and new tools for 2025

Online calculators, equity apps, and AI-powered research hubs are changing the buyout game. Platforms like futurecar.ai help drivers cut through noise and get unbiased, real-time data. Still, the best strategy is ongoing research, skepticism about dealer promises, and leveraging multiple resources for cross-checks.

Keep your information current. Market trends shift weekly, and what was true last month could change tomorrow. Self-advocacy isn’t just smart—it’s survival.

The last word: what you need to remember before your buyout

Key takeaways and final warnings

Lease buyouts in 2025 are neither a guaranteed jackpot nor a guaranteed trap. The only way to win is to verify every number, question every fee, and never accept the first answer. Emotional and financial stakes are high—this isn’t just a transaction, it’s a major life decision.

Revisit your motivations: Are you keeping your car for comfort, to beat the market, or because you’re avoiding hard choices? The answer should shape your strategy.

What most guides still get wrong

Many guides traffic in recycled advice: “Just compare prices” or “Negotiate hard.” That’s fine, but it misses the point—real leverage comes from understanding the system, spotting traps before they close, and staying skeptical of anyone selling a “sure thing.”

Empower yourself with knowledge, double-check every source, and lean on expert-driven platforms like futurecar.ai to stay sharp. The more you know, the less you risk.

In the end, the smartest car lease buyout decisions aren’t about luck—they’re about outsmarting a system that’s always evolving, and owning your outcome, whatever road you choose.

Sources

References cited in this article

- Car and Driver(caranddriver.com)

- Lease End 2025 Report(leaseend.com)

- LendingTree(lendingtree.com)

- Autotrader(autotrader.com)

- Consumer Reports(consumerreports.org)

- MSN(msn.com)

- BusinessWire(businesswire.com)

- USA Today(usatoday.com)

- Forbes(forbes.com)

- Lease End Press(leaseend.com)

- Bankrate(bankrate.com)

- Lease End Guide(leaseend.com)

- Bankrate(bankrate.com)

- NerdWallet(nerdwallet.com)

- CarLeases.org(carleases.org)

- Morningstar(morningstar.com)

- Golomb Legal(golomblegal.com)

- BusinessWire(businesswire.com)

- Reddit(reddit.com)

- Forbes(forbes.com)

- Debt.com(debt.com)

Find Your Perfect Car Today

Join thousands making smarter car buying decisions with AI

Frequently Asked Questions

What is a car lease buyout and why has it become more relevant in 2025?

A car lease buyout is when you purchase the vehicle you've been leasing at the end of your lease term. It has become increasingly relevant since the post-pandemic market created supply chain disruptions and chip shortages that drove up used car values, sometimes making the buyout price written into contracts years earlier suddenly much cheaper than current market prices. According to Lease End's 2025 report, consumer savings from buyouts reached $75.7 million in 2024 alone.

How much has the used car market changed since the pandemic?

The used car market experienced dramatic value spikes following COVID-19, with increases of 18% in 2020, 36% in 2021, and 22% in 2022 due to supply chain chaos and chip shortages. By 2024, the market had stabilized somewhat with a 6% increase, and by 2025 only a 2% increase, but the impact left many lessees with hidden equity in their vehicles.

What are typical new car prices and lease payment costs in 2025?

New car prices hit an average of $48,641 in March 2025, while monthly lease payments have ballooned past $700, making lease buyouts an increasingly attractive financial option for many drivers.

Are there restrictions on lease buyouts from all automakers?

No, while some automakers like Tesla had previously restricted buyout options, they have reinstituted buyout options after prior restrictions, indicating that lease buyout availability is expanding across the industry.

Continue Reading

Explore more from Smart car buying assistant

Car Lease Vs Buy in 2026: the Real Cost of Every Choice

Discover insights about car lease vs buy

The Dark Side of Car Lease Deals: What No Dealer Will Tell You

Car lease deals decoded: Expose hidden costs, master negotiation, and unlock 2026’s smartest deals. Don’t let slick ads outsmart you—transform your next lease.

Buying or Leasing a Car in 2026? Get the Raw Truth

Car leasing vs buying comparison—find out which wins in 2026. Unmask hidden costs, real savings, and the tech shifts reshaping your next big decision.

Inside Car Lease Transfer: What They Don’t Want You to Know

Car lease transfer secrets exposed: Discover how to swap your lease, dodge hidden traps, and save big with expert tips. Start your smarter car journey now.

Leasing or Buying? the Car Deal Myths You Still Believe

Car buying vs leasing pros and cons exposed: Discover the hidden traps and unexpected perks in 2026’s car market. Make a smarter choice today.

Car Lease Terms: What Dealers Won’t Tell You in 2026

Car lease terms decoded: Discover the 11 brutal truths, hidden costs, expert hacks, and future trends you need to know. Outwit the system—read before you sign.

Car Buying Vs Leasing Financial Analysis That Saves You Thousands

Discover insights about car buying vs leasing financial analysis

Is Trading in Your Car for a Lease Genius or a Trap?

Trade in car for lease smarter in 2026: Unmask hidden costs, dodge dealership traps, and master the art of switching to a lease with real-world data and expert insight.

Leasing a Car in 2026: What No One Tells You

How to lease a car without regrets: debunk myths, avoid traps, and get the best deal in 2026. Unfiltered guide with case studies, strategies, and expert tips.

Car Lease Types in 2026: the Traps, the Math, the New Options

Discover insights about car lease types

Lease Negotiation in 2026: Outsmart Dealer Tactics, Not Yourself

Discover insights about lease negotiation

Break Your Lease, Break the Rules: Car Buying Tips They Don’t Want You to Know

Car buying lease termination tips to avoid penalties, outsmart dealers, and win big. Discover expert secrets and real-world strategies for 2026. Start smarter now.